**Investing in the Stock Market: Lump Sum vs SIP – Understanding CAGR and Its Influence**

Engaging in stock market investments is widely regarded as one of the leading methods to enhance wealth over time. Nevertheless, novice investors frequently encounter a significant choice: should they invest a substantial sum initially as a lump sum or implement a Systematic Investment Plan (SIP) for consistent, smaller investments? To arrive at an educated choice, it’s crucial to grasp the concept of **Compound Annual Growth Rate (CAGR)**—a vital metric that assesses the growth rate of investments over time, taking compounding into account.

This article delves into CAGR, clarifies its calculation, and investigates reasons for its differences between lump sum and SIP investments. By the conclusion, you will be more prepared to select the investment strategy that fits your financial aspirations.

—

## **What is CAGR, and How is it Measured?**

CAGR, or **Compound Annual Growth Rate**, represents the yearly growth rate of your investment over a designated timeframe, integrating the effect of compounding. Compounding permits earnings to create additional returns, effectively allowing your wealth to “snowball” over time.

### **CAGR Calculation**

The computation for CAGR is as follows:

**CAGR = (Final Value of Investment / Initial Value of Investment) ^ (1 / Duration in Years) – 1**

### **Illustration**

Consider an investment of ₹1,00,000 that escalates to ₹1,61,051 after 5 years. To determine CAGR:

– **Initial Value:** ₹1,00,000

– **Final Value:** ₹1,61,051

– **Duration:** 5 Years

Applying the formula:

**CAGR = (₹1,61,051 / ₹1,00,000) ^ (1 / 5) – 1 = 12%**

This signifies that your investment advanced at an annualized rate of 12% annually over the span of 5 years.

—

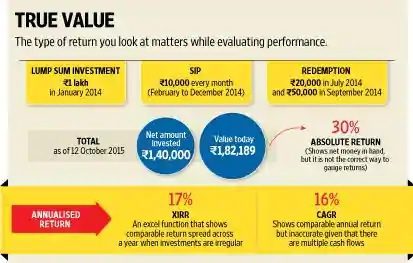

## **CAGR: Evaluating Lump Sum and SIP Investments**

### **1. Lump Sum Investments**

Lump sum investing entails placing a substantial, one-time amount into the market or an investment medium. For example, you might invest ₹5,00,000 in equity mutual funds in one go.

The main benefit of lump sum investing is that the entire sum is immediately subject to growth and compounding, potentially providing a superior return.

**Illustration:**

– **Invested Amount:** ₹5,00,000

– **Value After 5 Years:** ₹9,14,035

– **CAGR = (₹9,14,035 / ₹5,00,000) ^ (1 / 5) – 1 = 16.09%**

Thanks to the compounding effect, the initial ₹5,00,000 investment appreciated to ₹9,14,035 over five years, yielding a CAGR of 16.09%.

—

### **2. SIP Investments**

A Systematic Investment Plan (SIP) lets you invest a fixed, smaller amount monthly. For instance, you may choose to invest ₹10,000 each month for 5 years, summing up to ₹6,00,000. In this scenario, your funds are progressively introduced into the market.

While SIPs impart discipline to investing and assist in reducing market fluctuations (through rupee-cost averaging), the returns tend to be comparatively lower due to the staggered exposure of total capital to compounding.

**Illustration:**

– **Monthly SIP:** ₹10,000

– **Investment Duration:** 5 Years (60 Months)

– **Overall Investment:** ₹6,00,000

– **Final Value:** ₹8,92,800

– **CAGR = (₹8,92,800 / ₹6,00,000) ^ (1 / 5) – 1 = 13.44%**

In this case, a total SIP investment of ₹6,00,000 over 5 years increases to ₹8,92,800, leading to a CAGR of 13.44%.

—

## **Why Does Lump Sum Investing Produce a Higher CAGR?**

The elevated CAGR of lump sum investments is primarily due to two fundamental factors:

1. **Immediate Compounding Benefits:** The full principal begins earning returns right from the start, allowing compounding to exert a more significant influence over the years.

2. **Prolonged Market Exposure:** With a lump sum investment, the total amount has a longer duration in the market compared to SIPs, where additional contributions accumulate incrementally.

For instance, in a 5-year SIP, while the initial installment enjoys the maximum time for growth, later monthly contributions (such as those in the 4th or 5th year) have limited time in the market to gain from compounding.

—

## **Which Method is Superior – Lump Sum or SIP?**

The decision between lump sum and SIP hinges on