**Strategies for Efficient Retirement Spending: A Q&A Format**

Retirement marks a crucial phase of life, where intentional financial planning and spending techniques can guarantee sustainability and tranquility. This section tackles frequent inquiries related to the effective management and expenditure of retirement savings.

**Q1: How can I evaluate my retirement spending requirements?**

A1: Begin by reviewing your existing expenses to grasp your essential needs and discretionary costs. Take into account expenses that may change during retirement, like healthcare and travel, and factor in inflation. A thorough budget can clarify and assist in planning your withdrawals.

**Q2: What does the ‘4% Rule’ mean, and is it still applicable today?**

A2: The ‘4% Rule’ serves as a guideline indicating that retirees should withdraw 4% of their retirement savings each year. This rule is designed to sustain savings for 30 years. Nonetheless, due to market variations and longer life expectancies, it is advisable to assess this rule with a financial advisor to adapt it to contemporary economic conditions.

**Q3: In what ways can I enhance my Social Security benefits?**

A3: Postponing your Social Security benefits until age 70 can significantly boost your monthly payments. Assess your health, life expectancy, and financial requirements to determine the optimal time to begin receiving benefits, striking a balance between immediate needs and long-term advantages.

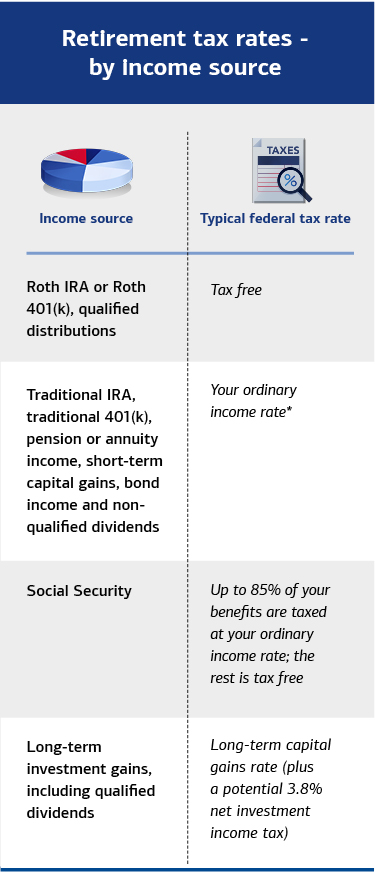

**Q4: What methods can help reduce taxes on retirement withdrawals?**

A4: Achieve tax diversification by employing various retirement accounts, such as Roth IRAs for tax-exempt withdrawals. Strategically plan your withdrawals across accounts to stay within lower tax brackets. It may be valuable to seek advice from a tax expert to maximize tax efficiency.

**Q5: How should I tackle healthcare expenses in retirement?**

A5: Prepare for healthcare costs by familiarizing yourself with Medicare options and potential expenses, including premiums, deductibles, and out-of-pocket costs. Look into supplemental insurance policies for extra coverage and keep a health savings account (HSA) if relevant.

**Q6: How can I modify my investments to suit retirement spending?**

A6: Transition to a more conservative investment strategy as retirement approaches, focusing on bonds and income-producing assets. Nevertheless, maintain a portion of growth-oriented investments to combat inflation. Regularly reassessing your portfolio is vital to align with your spending objectives.

**Q7: What measures can I take to guard my savings against inflation?**

A7: Designate a segment of your portfolio for investments that offer inflation protection, such as Treasury Inflation-Protected Securities (TIPS) or real estate. These assets can serve as a shield against inflation, preserving your purchasing power.

**Q8: How do annuities fit into a retirement spending strategy?**

A8: Annuities can deliver a guaranteed income for life, mitigating the risk of exhausting your savings. Consider incorporating them into your income stream while carefully evaluating the fees and terms to ensure they match your objectives.

**Q9: What strategies can I employ to manage debt as I enter retirement?**

A9: Make it a priority to eliminate high-interest debt before retiring, as a fixed retirement income can complicate debt management. Explore refinancing options to lower interest payments and increase cash flow.

**Q10: How frequently should I reassess my retirement spending plan?**

A10: Perform yearly reviews or whenever significant life changes occur, such as alterations in health or economic conditions. Consistent evaluations will facilitate timely adjustments, ensuring that your spending aligns with your changing circumstances.

Mindful and strategic planning is essential for enjoying a financially stable retirement. By addressing these elements and seeking professional guidance when needed, retirees can adeptly manage their spending and maintain their desired lifestyle throughout their golden years.