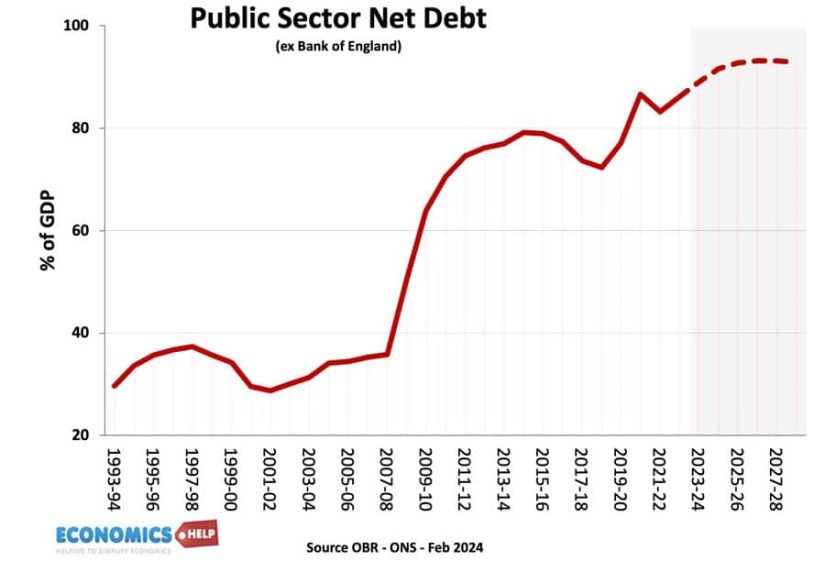

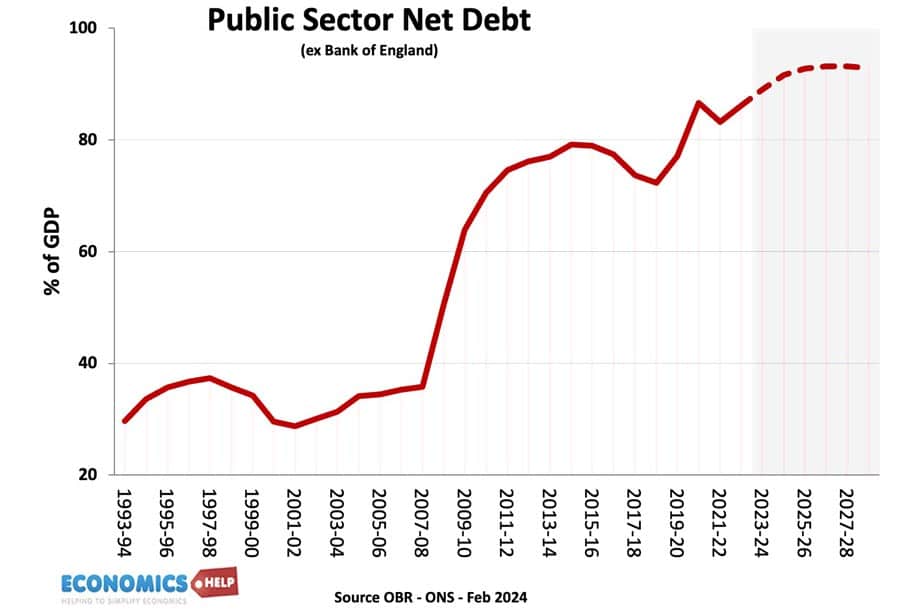

**Title: Comprehending the Present Condition of U.S. Household Leverage and Its Repercussions for Economic Stability**

In recent times, a prominent trend within the U.S. economy is the unprecedentedly low household leverage, presently at an 80-year low. This figure, underscored by the Federal Reserve Board, acts as a symbol of fiscal prudence among American households, marking a substantial change in consumer habits since the financial crisis of 2007-2009.

### The Lessons of the Past

The time preceding the financial crisis was marked by excessive household borrowing, chiefly in the form of mortgages and consumer debt. Numerous individuals accrued considerable leverage, presuming that escalating property values and accessible credit would persist indefinitely. Regrettably, when the market collapsed, millions were left jobless and witnessed a stark decline in their net worth, exposing the dangers of high leverage. Personal testimonies from those who experienced financial struggles reveal the emotional and economic impact of this crisis—dips of 35% to 40% in net worth were commonplace.

### A More Resilient Household Sector

Fast forward to the present, the diminished household leverage indicates that families are in a more secure position to endure economic downturns. With significant cash reserves and reduced debt levels, households can sidestep the frantic selling that characterized earlier downturns. In a recessionary climate, the assumption is that most households will prefer to “hunker down” rather than liquidate their assets at reduced values.

The current strength of household finances creates avenues for strategic investments during market corrections. The likelihood of V-shaped recoveries appears more feasible with households possessing cash reserves and diminished debt responsibilities. Reports suggest that many homeowners now experience the comfort of owning their properties outright—around 40% of U.S. homeowners are mortgage-free. This robust foundation provides greater financial flexibility and stability.

### The Only Good Type of Leverage

While it is evident that reduced overall debt is advantageous, strategic leverage can still contribute to wealth creation, particularly in a bull market. However, not all debt is equally beneficial. Consumer debt, mainly high-interest credit card debt, presents substantial financial hazards and should be avoided. On the other hand, mortgage debt, when judiciously used to acquire real estate, can promote long-term wealth building.

Holding a primary residence can offer both appreciation potential and a stable living environment, frequently surpassing the returns from savings and investments that individuals might pursue instead of purchasing a home. Furthermore, as many homeowners secured favorable mortgage rates during periods of low interest, the threat of another housing-related crisis is significantly reduced.

### Recommended Asset-to-Debt Ratios

To assess financial wellness, individuals can adopt a guideline of suggested asset-to-debt ratios. Aspiring to a 5:1 ratio during one’s peak earning years can pave the way for a comfortable retirement. This ratio ensures that obligations are manageable and linked to appreciating assets, enabling individuals to navigate economic adversities without excessive strain. For those approaching retirement, the focus should shift toward achieving a debt-free status, ideally attaining a 10:1 asset-to-liability ratio for optimal peace of mind.

### The Transition from Maximization to Simplicity

As individuals age, the focus on maximizing financial gains often transitions to a preference for simplicity and clarity. People may discover that once they have dispensed with significant debts, their attention turns to stability instead of relentless wealth accumulation. Embracing this change can foster a more rewarding and less anxiety-ridden approach to personal finance.

### Conclusion

Today’s historically low U.S. household leverage is indicative of a wider economic resilience, molded by valuable lessons from former financial crises. As families chart their financial paths, comprehending the intricacies of debt and employing strategically sound practices can nurture financial stability and tranquility. Shifting towards a managed leverage approach, alongside continued asset diversification, will strengthen the capacity to endure economic fluctuations while striving for lasting financial independence.