2025 Has Laid the Groundwork—Now Let’s Discuss 2026

In spite of challenges such as elevated interest rates, tariff concerns, geopolitical strains, and a U.S. government shutdown, 2025 is wrapping up robustly. Barring an extended market downturn, we can expect a third consecutive year of double-digit increases, a milestone not achieved since the late ’90s.

Canadian dividend investors should take note:

Canada is outpacing the U.S.—and it’s not because of AI.

While growth in the U.S. is driven by traditional tech sectors, Canada’s TSX has flourished due to three primary reasons:

- Gold stocks surged, significantly enhancing the basic materials sector.

- Banks and insurers bounced back robustly, propelled by improved earnings and financial health.

- Industrials and utilities benefitted from the global AI surge, driven by heightened data-center development and energy requirements.

Consumer staples and REITs have remained stagnant, creating opportunities for patient dividend investors as we approach 2026.

To access comprehensive charts and analysis, download the complete 2025 Market Commentary within the Top 7 Stocks Booklet to also discover stock suggestions for your purchasing list!

{kind=link}

This enlightening 16-page guide encompasses:

- A detailed review of the 2025 stock market to understand the landscape beyond stock options.

- A clear, repeatable methodology leveraging the Dividend Triangle (revenue, earnings, dividend growth).

- Seven highly-convicted stocks chosen based on solid fundamental metrics.

Make 2026 your most successful investment year—download the complimentary PDF featured in the article.

The current blend of sector disparity and macroeconomic contradictions lays the groundwork for selecting 2026’s prime Canadian dividend stocks. With this backdrop, here are three essential holdings that resonate with the trends influencing the Canadian market.

Top 3 Canadian Dividend Stocks for 2026

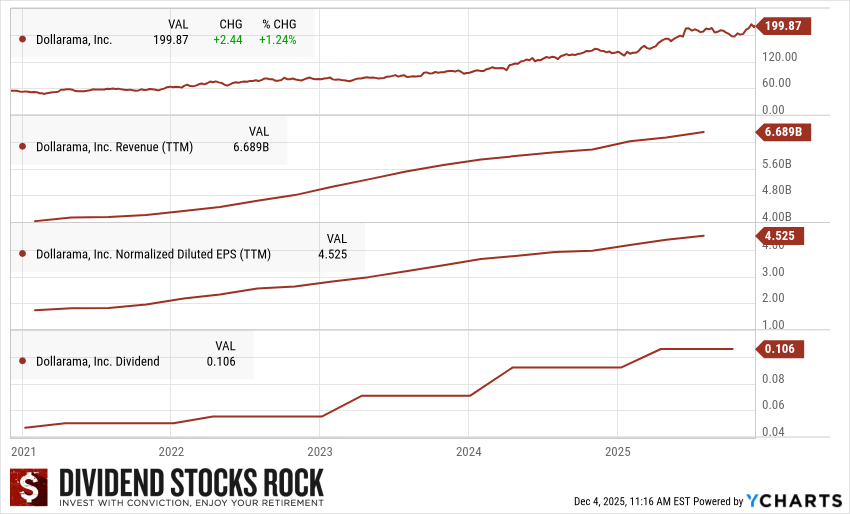

Dollarama (DOL.TO) — A Fundamental Compounder

Dollarama distinguishes itself as a Canadian stock with a well-established long-term narrative. In times of budget constraints and e-commerce competition, it serves as a refuge for budget-conscious consumers.

Its reliability is noteworthy:

- Growing same-store sales.

- Consistent new store launches.

- Enhanced private-label market share increases profitability.

- The new $5 pricing amplifies Dollarama’s pricing power.

Dollarama’s prospects include the expansion of Dollar City in Mexico and acquiring Australia’s Reject Shop. These initiatives extend DOL’s growth potential beyond Canada, which is unusual for Canadian retailers.

An exemplary instance of a defensive, efficient growth stock—Dollarama is still undervalued by the market.

{kind=link}