Constructing a retirement portfolio revolves around establishing a sustainable income source.

The widespread belief is that achieving the highest yield guarantees success. In truth, success is realized by crafting a portfolio that provides persistent cash flow while protecting or enhancing your capital during market fluctuations.

This drives the purpose of the Dividend Income for Life Guide, a resource aimed at offering a retirement income strategy resilient against market instability.

Access the Dividend Income for Life Guide for free here.

Continue reading for a deeper understanding of what the guide entails.

The Concealed Dangers of High Yield

A yield between 6% and 7% might appear to be an easy route to retirement income:

- Acquire stock

- Receive dividends

- Cover expenses

This straightforward approach overlooks a critical market warning: high yields can indicate limited growth potential. Growth stagnation may threaten dividend consistency, resulting in lost income and capital.

Analysis of high yields over ten years disclosed:

- Noticeable negative total returns were documented despite the dividends received.

- Regular dividend reductions.

- A significant number of companies did not match inflation with their dividend increases.

This does not constitute sustainable income; it reflects a deteriorating portfolio over time, compelling unwanted retirement decisions.

My analysis substantiates this finding.

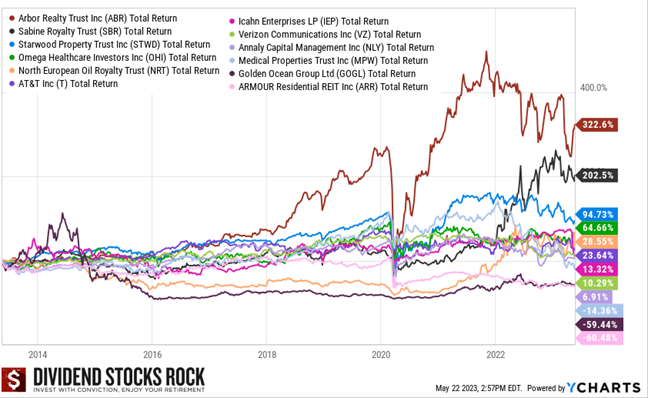

Celebrating a decade in 2023, I utilized the Dividend Stocks Rock stock screener to identify high-yield (4-5%) stocks over a span of ten years. The period from 2013 to 2023 exhibited low interest rates and economic growth, fostering a favorable environment for business.

Several well-known US companies reveal these patterns.

{kind=link}

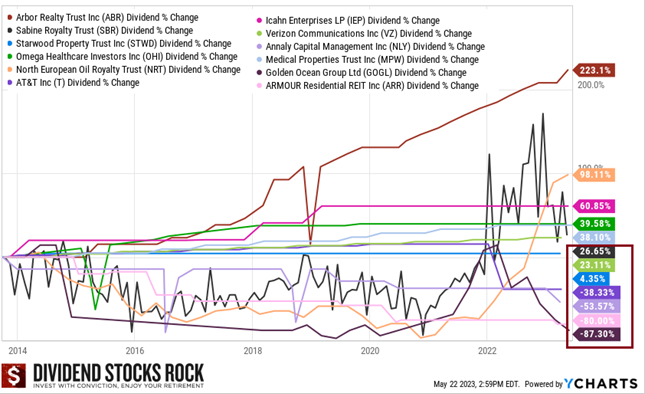

Initial assessments might seem positive, but it’s essential to analyze their dividend growth.

{kind=link}

My selection process and findings are detailed in the Dividend Income for Life Guide. Download it here.

Dividends vs. Dividend Growth

Dividends are not complimentary; they symbolize cash redistributed from company to shareholder due to limited internal investment options. Established, slow-growing firms frequently provide higher yields.

The real value lies in owning companies that consistently boost revenue, earnings, and dividends.

This concept forms the basis of dividend growth investing, as emphasized in the Dividend Triangle:

- Revenue growth

- EPS growth

- Dividend growth

These indicators are vital for ensuring retirement income that keeps pace with inflation over time.

Rethinking Low Yield

The primary worry for retirees is:

“I don’t want to sell shares.”

It’s completely understandable; no one desires to dismantle their portfolio to support retirement.

Nevertheless, possessing robust companies transforms selling shares into an asset rather than a drawback.

Low-yield,