Certain stock comparisons can be quite simple. One company may possess a more robust balance sheet, superior growth potential, or a more reliable business model.

Visa and Mastercard do not fall into the category of straightforward comparisons.

This scenario involves a competition between two leading companies operating high-caliber models in the marketplace. Both are integral to worldwide commerce. They both gain from the move away from cash, produce substantial margins, and demonstrate the type of Dividend Triangle that draws in dividend growth investors.

The crucial question isn’t if Visa or Mastercard operates as a good business—they both do. The real inquiry is which company should find a place in your investment portfolio at this moment.

Two Outstanding Companies Built on a Common Basis

Visa and Mastercard are frequently described as payment processors, yet this term does not adequately express the strength of their model. A more appropriate comparison would be to consider them as toll roads for international transactions.

When a customer makes a purchase and a merchant receives payment, Visa or Mastercard securely and almost instantaneously manages the money transfer, earning a fee without taking on credit risk, which remains with the issuing bank.

This framework is exceptionally attractive.

They profit from card payments, digital wallets, contactless transactions, e-commerce, and overseas transactions, without engaging in direct lending. It’s a setup that requires minimal assets while achieving vast scale. As transaction volumes increase, revenue ascends without necessitating hefty capital investments, resulting in highly scalable and margin-rich enterprises.

Both companies possess numerous growth pathways. The global transition to electronic payments is ongoing, with cross-border spending acting as a significant engine of growth. Emerging markets present abundant prospects for converting cash transactions to digital methods. Furthermore, both firms have branched into value-added services such as fraud prevention, analytics, digital verification, open banking, consulting, and payment gateways.

This variety provides several growth drivers.

The Strength of the Moat

Visa and Mastercard feature one of the most formidable market moats.

Their network effect is substantial: consumers utilize them because merchants accept them, and merchants endorse them because consumers use them. Banks issue cards through these networks due to their established scale, creating a self-perpetuating cycle that’s challenging for competitors to penetrate.

This moat is reinforced by high switching costs, worldwide acceptance, technological infrastructure, regulatory barriers, and consumer trust. Constructing a competing entity with comparable reach would demand considerable capital, time, and effort.

This often leads to higher valuations for companies with strong market positions, substantial cash flow, and enduring growth potential.

Distinctions Between Visa and Mastercard

While the companies may appear alike, a closer examination uncovers key differences.

Visa dominates in size, boasting a broader footprint and a stronger position in the U.S. debit market. Its emphasis leans more towards consumer card spending and cross-border travel, backed by superior margins that grant flexibility in legal expenses, business investments, and shareholder returns.

In contrast, Mastercard positions itself as a growth challenger, offering a wider range of value-added services and a stronger focus on partnerships, international markets, and digital-first strategies. It has established strong footholds in various non-U.S. regions and often actively pursues new ventures.

This nuanced difference matters.

Visa shines in scale and efficiency, while Mastercard flourishes through innovation and service diversification.

In summary: Visa is the scale powerhouse; Mastercard is the growth integrator.

The Argument for Dividend Growth

Both firms are particularly attractive to dividend growth investors.

Visa and Mastercard may not be high-yield stocks, but that is acceptable. The focus is on owning businesses capable of remarkable revenue, earnings, and dividend growth over the long haul.

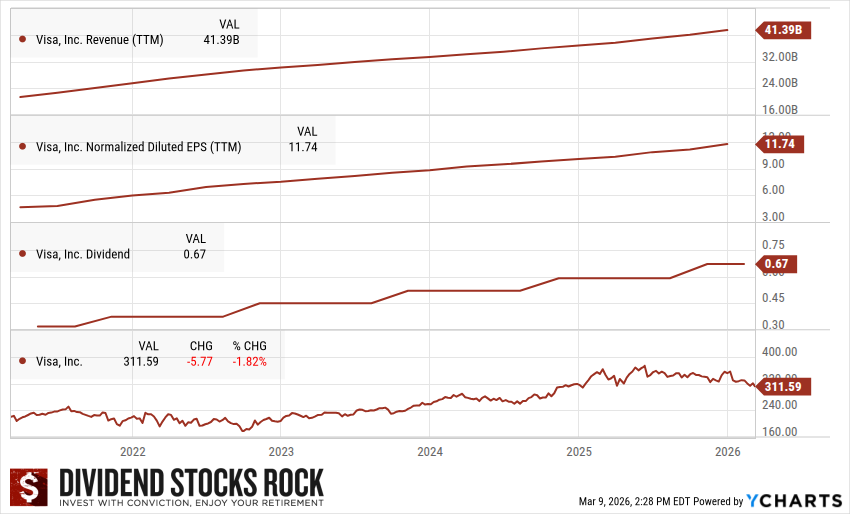

Their Dividend Triangles substantiate this.

With payout ratios comfortably below 30%, there is plentiful capacity for future dividend increases, buoyed by earnings growth. Revenue trends emphasize the robustness of the business model, creating a conducive environment for compounding as time progresses.

{kind=link}

The charts for both companies present a compelling argument. Visa’s 5-year Dividend Triangle highlights consistent revenue growth, strong EPS advancement, and disciplined dividend escalations. Mastercard, which showcases slightly superior long-term growth, enhances its dynamic appeal even with Visa being