**Investing in the Futures of Children: Leveraging the Gift Tax Cap**

Every couple of years, the stock market experiences upheaval, often leading to stress for investors. Observing portfolio declines can create a feeling of powerlessness, but for parents, that sensation can transform into proactive measures. This past year, amid geopolitical issues affecting the financial markets, I made a decisive move: I invested significantly beyond the annual gift tax cap into my children’s custodial investment accounts.

Since they were born, I have directed the gift tax limit into these accounts, which include 529 plans and custodial accounts. This approach has formed a key aspect of my wealth accumulation strategy, offering my children a strong financial cushion. Even with a market decline, I continued my investments, contributing approximately $35,000 for each child, exceeding the usual limit of $19,000.

Although this may not represent the most advantageous tax plan, the emotional fulfillment of taking assertive measures felt appropriate. By investing in my children’s futures, I chose to act rather than remain passive, particularly when their portfolios encountered downturns. For numerous American families, surpassing the gift tax cap is less intimidating than it appears.

### Grasping the Gift Tax Cap

The annual gift tax exclusion is established at $19,000 per recipient in 2026, generally increasing modestly due to inflation. Notably, exceeding this threshold does not immediately invoke tax obligations; rather, it necessitates filing IRS Form 709, reporting the gift without incurring taxes. The extra amounts are subtracted from a generous lifetime gift tax exemption, which is $15 million per individual in 2026. As a result, most individuals seldom confront direct gift tax bills.

### The Process of Gift Tax Filing

For gifts that go beyond the annual exemption, Form 709 must be submitted by April 15 of the following year. This form records the gift and indicates any portion beyond the annual limit, enabling the IRS to monitor total gifts. Usually, married couples can pool their exclusions, allowing for a total of up to $38,000 per recipient tax-free.

Neglecting to file Form 709 does not typically result in penalties if no gift tax is actually owed, highlighting the self-reporting nature of the system. Nevertheless, it is advisable to file in order to maintain clarity and keep the statute of limitations intact.

### Proactive Financial Choices

If the estate value is below the lifetime tax threshold, the ramifications of exceeding the annual gift tax limit are negligible. Most families are unlikely to reach that threshold, making the primary concern the completion of Form 709 instead of fretting over tax liabilities.

For me, this year’s contributions were intended not only for tax strategy but also to address current market realities. Motivated by the long-term prospects of my children’s investments, I concentrated on proactive contributions knowing that recovery is on the horizon.

### Establishing Goals for Custodial Accounts

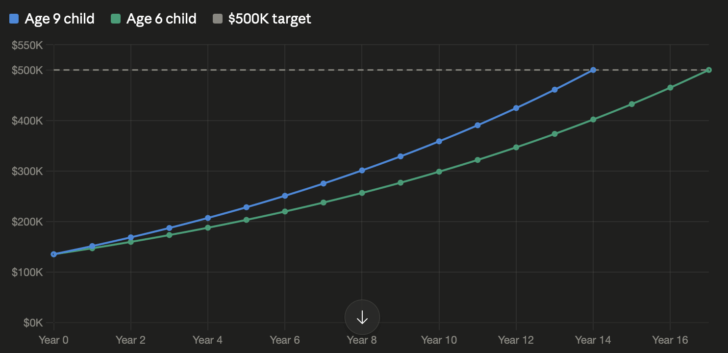

Defining a target for my children’s custodial investment accounts is essential. My goal is to accumulate $500,000 for each child by their college graduation, creating significant prospects for their futures. Assuming a 7% average return, calculated annual contributions will stay within the gift tax limit, streamlining the funding process.

The equity already existing in these accounts will considerably help in achieving that goal. Market variations will affect results, but adhering to a disciplined and consistent investment approach is crucial.

### Embracing Financial Independence Through Gifts

Gift tax laws are designed to ensure wealth is transitioned responsibly among generations, not to impede parental support for children. If you find an opportunity to invest beyond the annual limit during market downturns, view it as a worthwhile approach. Just file Form 709 and keep track of your lifetime exemption utilization.

With years of compounding potential ahead, investing vigorously for your children during market declines can be one of the smartest financial strategies available. By nurturing investment growth today, you can create a significant legacy for future generations.

In summary, as someone dedicated to financially empowering my children, I urge others to consider how they can exploit gift tax opportunities to benefit their families. Investing in your children’s futures transcends mere financial decision-making; it constitutes a legacy that can empower them for years to come.