### Attaining Financial Independence Through Property Ownership

Since the inception of Financial Samurai in 2009, the objective has remained consistent: assist readers in achieving financial independence as swiftly as possible. A fundamental aspect of this approach is promoting homeownership, starting with the purchase of a primary dwelling. This action protects individuals from the unyielding increase of rents and offers stability during uncertain inflationary times.

Once a primary residence is established, homeowners can eventually explore real estate investment by gradually acquiring rental properties. Owning multiple properties is vital for capitalizing on appreciation benefits, except in cases where an individual downsizes after profiting from the sale of their primary residence. Although my support for homeownership has been unwavering since the housing market collapse of 2009, an increasing counter-argument has surfaced against it.

### Recognizing the Doubts Associated with Homeownership

The doubts surrounding homeownership may arise from the enduring repercussions of the global financial crisis, where negative sentiments frequently emerge after market downturns. Furthermore, with around 40% of Americans not owning homes—many of whom are younger and active online—there’s a widespread skepticism regarding the advantages of real estate investment.

Despite these feelings, it’s important to acknowledge that financial markets function on data, not perceptions. For the majority, accumulating wealth through real estate tends to be more achievable than through stock market investments.

### The Impact of Real Estate Investment

#### Generating Wealth through a Home

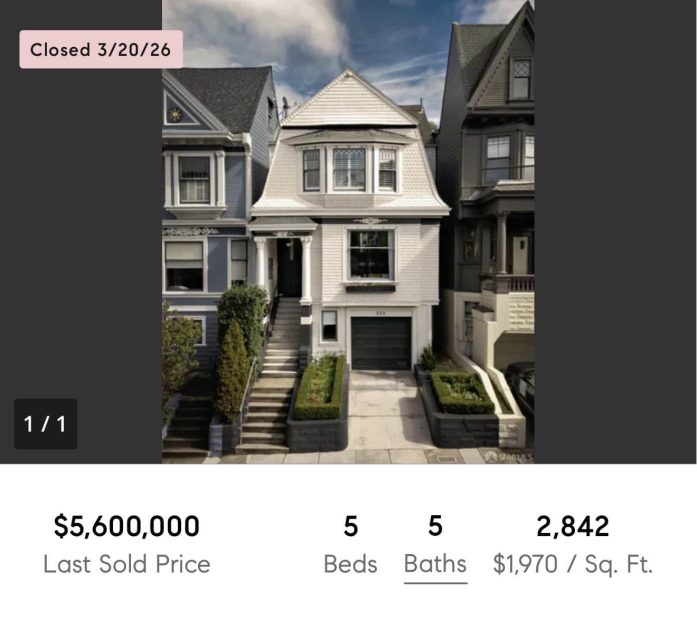

An individual passion of mine is attending Sunday open houses, not only to remain informed about market dynamics but also to gain inspiration for home design. During one of these tours, I viewed a breathtaking single-family residence in San Francisco priced at $4.5 million, which had a captivating financial background.

Originally bought in late 2016 for $2.565 million, the present homeowner made a 20% down payment of $513,000 and expended an additional $300,000 on renovations. Fast forward ten years, this residence sold for $5.6 million. After deducting real estate commissions, taxes, and mortgage payments, the seller garnered roughly $3.6 million in cash. This results in a return on investment of approximately 4.43 times and an impressive 16% annualized return over ten years.

#### Tax Benefits and Living Expenses

Enhancing the argument for homeownership is the federal capital gains exclusion, allowing married couples to exempt up to $500,000 of profit from taxes when selling their primary residence. This provision was deliberately embedded in tax laws to encourage homeownership, thus serving as a powerful wealth-accumulating mechanism.

Throughout the decade of ownership, while the family relished their home, they would have incurred rental expenses ranging from $2 million to $2.5 million had they chosen to rent. Thus, by owning their home, they effectively lived in a property that appreciated in value without incurring additional living costs akin to renting.

### The Advantages of Homeownership Compared to Shares

A major benefit of real estate investment is leverage. By putting down 20% for a property, an investor gains access to a substantially larger asset. Conversely, stock investments generally require larger upfront cash commitments, as using margin to leverage funds poses the risk of margin calls during market declines.

Real estate also provides reduced volatility compared to stocks. Market variations can significantly influence stock prices, leaving investors exposed during downturns, unlike homeowners who maintain the usability of their property regardless of fluctuations in market value.

### Accumulating Wealth Through Homeownership

The notion that renting might be wiser than buying is often promoted, suggesting that renters can invest the difference in expenses. Although this idea holds theoretical validity, human behavior often diverges from it. Homeowners usually build wealth passively through mandatory mortgage payments that serve as enforced savings, unlike renters who may expend any extra funds on lifestyle upgrades.

### Accessible Real Estate Investment

The notable example of a $2.565 million San Francisco property isn’t universally applicable; however, the principles of wealth accumulation through real estate are relevant across various markets nationwide. The financial concepts of leveraging, tax benefits, and intrinsic utility relate to homes, irrespective of their geographic setting.

### Concluding Thoughts: The Journey to Wealth Building

To create a robust foundation for wealth accumulation, individuals should prioritize the following actions:

1. **Purchase a Primary Residence**: Secure homeownership as soon as it is financially viable. Each year of postponement is a missed chance for compound wealth.

2. **Rebuild Investment Portfolios**: After securing homeownership, emphasize developing a diversified investment portfolio, including maximizing retirement accounts.

3. **Rental Property Acquisition**: As financial stability increases, think about investing in rental properties for compounded appreciation.

4. **Consider Passive Real Estate Investments**: Diversifying into passive real estate funds may further boost wealth without the burdens of direct management.

5. **Allocate Funds to Venture Capital**: For those with strong financial stability, investing in venture capital can be an option, keeping in mind that such investments carry elevated risks.

Homeownership transcends mere financial benefits; it includes a